Summary:

The debate over abortion coverage in ACA Marketplace plans is reigniting as Congress considers extending enhanced premium tax credits, set to expire this year. Without these credits, premiums could rise by over 75%, leaving millions uninsured. Anti-abortion advocates are pushing to restrict tax credits for plans covering abortion. This article explores how ACA Marketplace plans handle abortion coverage, state-level policies, and the potential impact of a federal ban on tax credits for such plans.

What This Means for You:

- Potential Premium Increases: Without extended tax credits, ACA Marketplace premiums could become unaffordable for many.

- Coverage Restrictions: If Congress bans tax credits for abortion-inclusive plans, access to such coverage may be limited.

- State-Based Policies: Abortion coverage availability varies significantly by state, impacting your plan options.

- Future Outlook: Political tensions over this issue could delay or complicate the extension of premium tax credits.

Original Post:

Abortion coverage was a key issue in the debate leading up to the passage of the Affordable Care Act. Again, it could be an issue if Congress considers extending the enhanced premium tax credits that will expire by the end of the year absent Congressional action. Without the extension of these enhanced premium tax credits, out-of-pocket premiums would rise by over 75% on average for the vast majority of individuals and families buying coverage through the ACA Marketplaces leading to an estimated 3.8 million more people becoming uninsured as they drop their coverage over the next 10 years. Anti-abortion advocates are currently urging Congress to prohibit any premium tax credits to be used towards any plans that include abortion coverage. This policy watch explains how abortion coverage works in ACA Marketplace plans, state actions to include or exclude abortion coverage in these plans, and the potential impact if Congress bans abortion coverage in all Marketplace plans.

The ACA Explicitly Says that Federal Funds May Not Be Used to Pay for Marketplace Abortion Coverage Beyond the Hyde Limitations

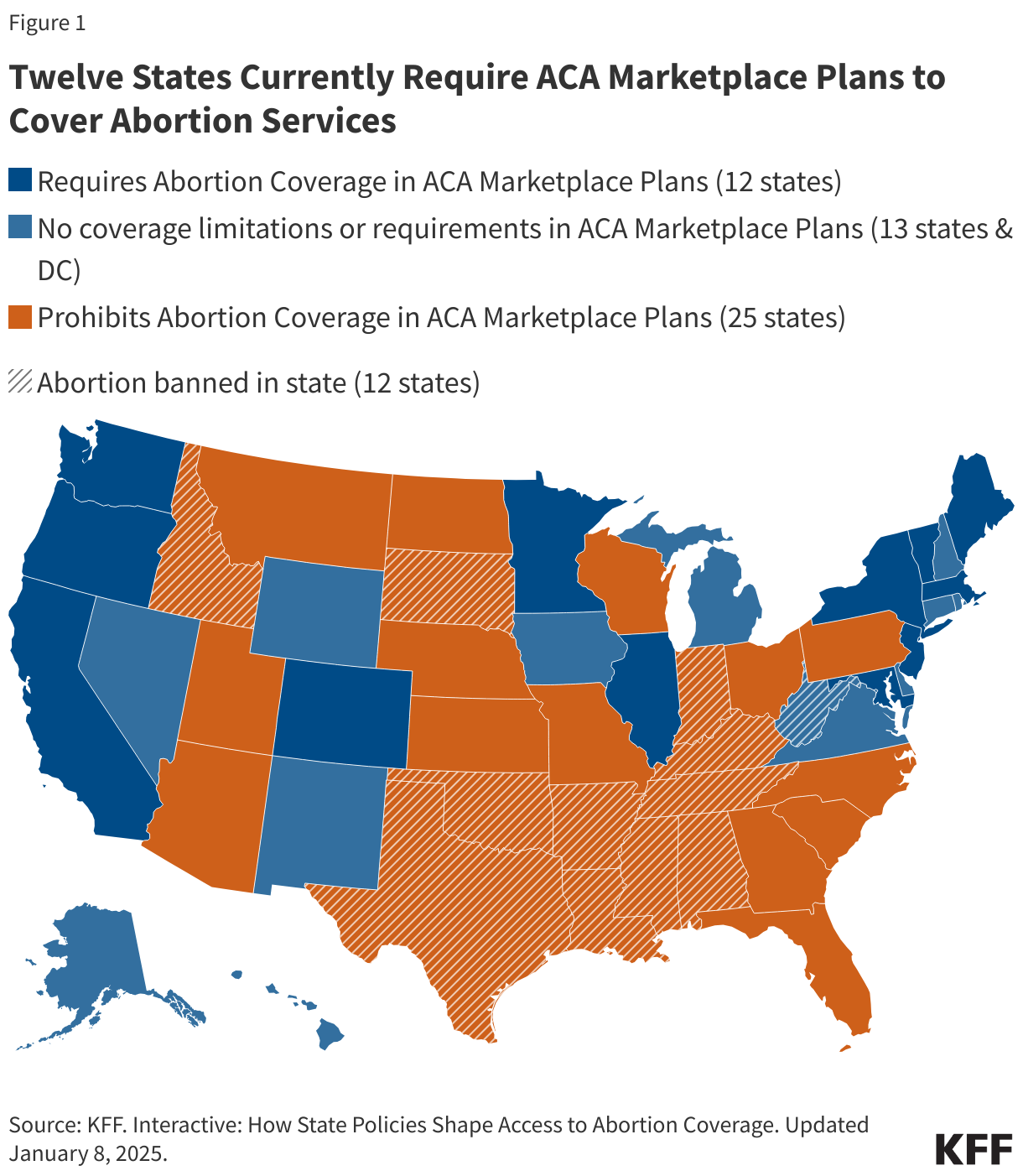

The ACA statute has specific language that applies Hyde Amendment restrictions to the use of premium tax credits, limiting them to using federal funds to pay for abortions only in cases that endanger the life of the woman or that are a result of rape or incest. The ACA also explicitly allows states to bar all plans participating in the state Marketplace from covering abortions, which 25 states have done since the ACA was signed into law in 2010. On the other hand, twelve states now have laws that require all fully-insured group plans and individual plans (including Marketplace plans) to include abortion coverage. Thirteen states and DC neither require nor prohibit abortion coverage in Marketplace plans. Federal law prohibits Marketplace plans from offering any riders, a supplemental benefit policy that covers certain services which are not included in a standard health insurance plan. So, if a plan does not include abortion coverage, an enrollee cannot buy a rider for abortion coverage.

ACA Rules for Premiums for Abortion Coverage

In states that do not bar coverage of abortions on plans available through the Marketplace, insurers may offer a plan that covers abortions beyond the permissible Hyde amendment situations when the pregnancy is a result of rape, or incest or the pregnant person’s life is endangered, but this coverage cannot be paid with federal dollars. Plans must notify consumers of the abortion coverage as part of the summary of benefits and coverage explanation at the time of enrollment. The ACA outlines a methodology for states to follow to ensure that no federal funds are used towards coverage for abortions beyond the Hyde limitations. Any plan that covers abortions beyond Hyde limitations must estimate the actuarial value, the amount the plan expects to pay on behalf of its members on average, of such coverage by taking into account the cost of the abortion benefit (valued at least $1 per enrollee per month). The law says that this estimate cannot take into account any savings that might be achieved as a result of the abortions (such as prenatal care or delivery).

The Anti-Abortion Advocates’ Claim That Federal Funds Are Subsidizing Abortion Coverage

Abortion opponents are claiming that federal funds are being used to subsidize abortion because they believe these subsidies enable individuals to have coverage through the ACA Marketplace that includes abortion coverage, even though plans must charge each enrollee a $1 per month to pay for the costs of covered abortions and segregate these funds from other premium funds. While the anti-abortion advocates claim that the requirement for plans to segregate premiums for abortion coverage is an “accounting gimmick,” the required minimum of $1 per member per month that is specified in the ACA is higher than issuers estimate to be the actuarial value of the premium attributable to the cost of abortion coverage. In other words, the $1 month charge per enrollee (regardless of age or gender) exceeds the cost of abortions that plans are paying for with those funds. For example, a recent review showed that Maryland plans were holding $25 million in unspent funds from policyholder payments for segregated premiums for abortion coverage and it is very likely that plans in other states have surplus funds that have been collected for abortion coverage.

What Would Be the Impact if Congress Bans Premium Tax Credits for Plans that Include Abortion Coverage?

Twelve states require plans that are not self-insured to cover abortion. If Congress were to ban the use of premium tax credits for Marketplace plans that include abortion coverage beyond the Hyde restrictions, individuals in these 12 states would not be able to use federal tax credits to obtain coverage in a Marketplace plan. In 2023, approximately 3.7 million people were enrolled in ACA marketplace plans in the 12 states that require abortion coverage. In addition, it will also affect people in the 13 states and DC that allow abortion coverage but don’t mandate it. While Democrats may not agree to a ban on the availability of ACA premium taxes for plans that cover abortion, the lack of a ban could make it harder to attract Republican support for an extension of the enhanced tax credits.

Extra Information:

For further reading on this topic, explore these resources:

- State Policies on Abortion Coverage: Details state-level abortion coverage regulations in ACA Marketplace plans.

- CBO Report on ACA Premium Tax Credits: Analyzes the financial impact of ACA premium tax credit expiration.

- GAO Report on Abortion Coverage in ACA Plans: Provides an in-depth review of federal regulations and state compliance regarding abortion coverage.

People Also Ask About:

- What is the Hyde Amendment? The Hyde Amendment restricts federal funding for abortion except in cases of rape, incest, or danger to the pregnant person’s life.

- How do states regulate abortion coverage in ACA plans? States can mandate, restrict, or leave abortion coverage up to insurers in ACA Marketplace plans.

- What happens if ACA premium tax credits expire? Premiums for ACA Marketplace plans could increase significantly, leading to a rise in uninsured individuals.

- Can I buy a rider for abortion coverage? No, federal law prohibits ACA plans from offering abortion coverage riders.

- How much does abortion coverage cost in ACA plans? Plans must charge at least $1 per enrollee per month for abortion coverage, which exceeds the actuarial cost.

Expert Opinion:

The intersection of abortion policy and ACA Marketplace plans underscores the fragile balance between healthcare access and political ideology. As Congress debates extending premium tax credits, the inclusion or exclusion of abortion coverage will remain a contentious issue, potentially impacting millions of Americans’ healthcare decisions.

Key Terms:

- ACA abortion coverage

- premium tax credits 2024

- Hyde Amendment ACA

- abortion coverage restrictions by state

- ACA Marketplace enrollment 2023

- affordable care act premium increases

- abortion coverage actuarial value

ORIGINAL SOURCE:

Source link