Summary:

Medicare Advantage has seen significant growth, with over half of eligible Medicare beneficiaries now enrolled in private plans. While enrollment growth slowed in 2025, the trend is expected to continue, impacting both beneficiaries and healthcare providers. Key differences between Medicare Advantage and traditional Medicare include prior authorization requirements, provider networks, and out-of-pocket costs. Hospitals, particularly in rural areas, have raised concerns about payment rates, delays, and denials, which could affect their financial stability as Medicare Advantage expands.

What This Means for You:

- Understand Prior Authorization: Most Medicare Advantage plans require prior authorization for hospital stays and other services, which can delay care. Be prepared to navigate these requirements.

- Review Provider Networks: Medicare Advantage plans often have restricted networks. Verify that your preferred providers are in-network to avoid higher costs.

- Monitor Out-of-Pocket Costs: Out-of-network care can be significantly more expensive. Plan accordingly to manage potential expenses.

- Future Outlook: As Medicare Advantage enrollment grows, anticipate potential changes in healthcare access, costs, and provider availability, especially in rural areas.

Original Post:

Enrollment in Medicare Advantage has grown rapidly in recent years, with more than half of all eligible Medicare beneficiaries now receiving their coverage from a private plan. Although the pace of enrollment increases slowed in 2025, the total number of Medicare Advantage enrollees still increased and the share of Medicare beneficiaries who obtain their Medicare benefits from a private plan is expected to continue to grow over the next decade. This trend has implications for beneficiaries and health care providers, including hospitals, because Medicare Advantage differs from traditional Medicare in many ways.

For hospitals and beneficiaries, one key distinction is that virtually all Medicare Advantage enrollees are in a plan that requires prior authorization for inpatient hospital stays (96%), post-acute skilled nursing facility stays (99%) and home health care (91%). Prior authorization is intended to reduce unnecessary care and lower costs, but it also imposes administrative burdens on providers, and sometimes leads to delays and barriers to care. Medicare Advantage plans also typically establish provider networks and impose higher out-of-pocket costs for out-of-network care. In light of the reported uptick in utilization among some Medicare Advantage enrollees, insurers looking to protect profits and guard against losses may seek to cut costs in ways that could impact hospitals, such as by tightening networks to direct patients to providers with lower costs. As Medicare Advantage enrollment grows, decisions made by insurers (related to networks, payment rates, prior authorization, and denials) along with decisions made by hospitals (whether to be in a Medicare Advantage network) can be expected to affect a larger share of the Medicare population.

Recently, hospitals and other providers—including in rural areas—have raised concerns about the impact of Medicare Advantage on their finances. Some hospitals have terminated contracts over payment rates, delays in payment, more restrictive coverage determinations, and denials. One issue that has drawn scrutiny from these groups has been plans’ practice of shifting hospitalized patients to “observation status,” which often means lower payments to hospitals and higher costs for patients. Additionally, one study estimated that Medicare Advantage denials of inpatient services reduced provider revenue by approximately 7%.

This data note examines the growth of Medicare Advantage as a share of hospital inpatient days between 2015 and 2023 based on cost reports submitted by hospitals to the Centers for Medicare and Medicaid Services (CMS).

Key Takeaways

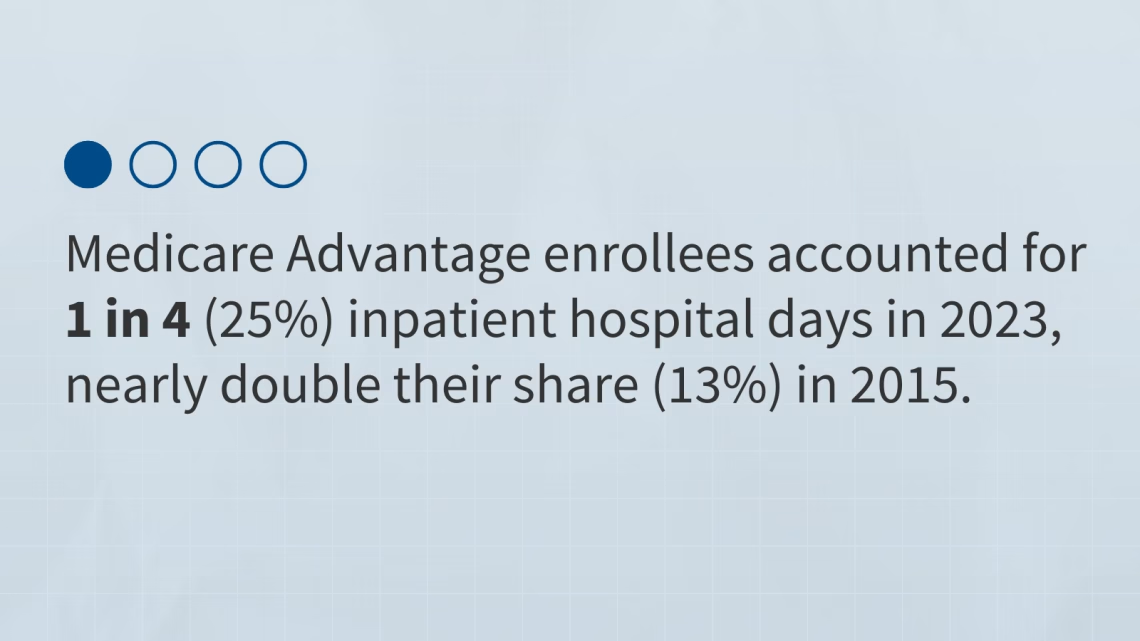

- Medicare Advantage represents a growing share of total hospital inpatient days. Medicare Advantage grew from 13% to 25% of total inpatient hospital days between 2015 and 2023, and as of 2023, half (50%) of all Medicare inpatient hospital days were attributed to Medicare Advantage enrollees.

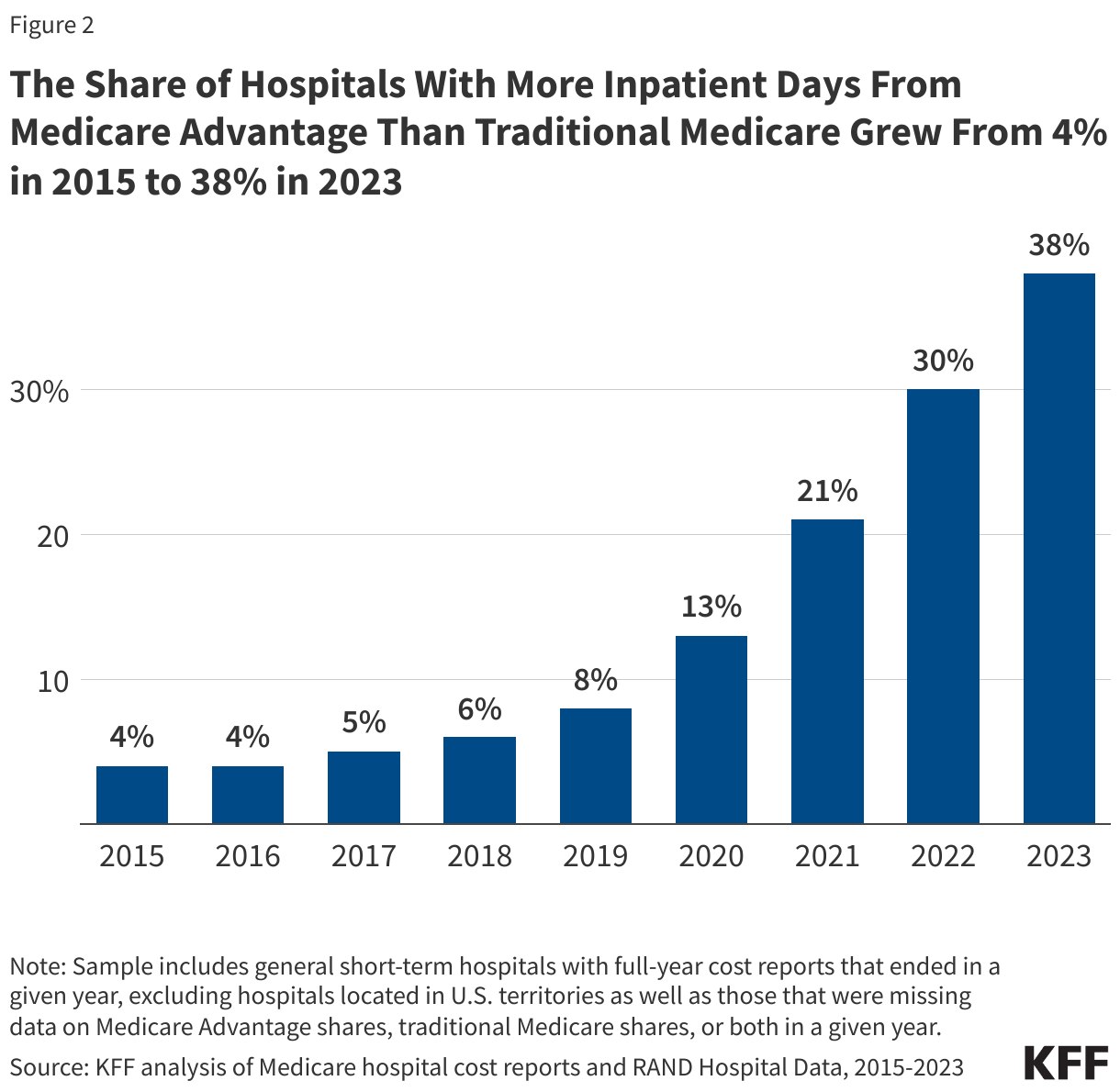

- Nearly four in ten hospitals had more inpatient days from Medicare Advantage enrollees than traditional Medicare enrollees in 2023. The share of hospitals with more Medicare Advantage than traditional Medicare inpatient days grew from 4% in 2015 to 38% in 2023.

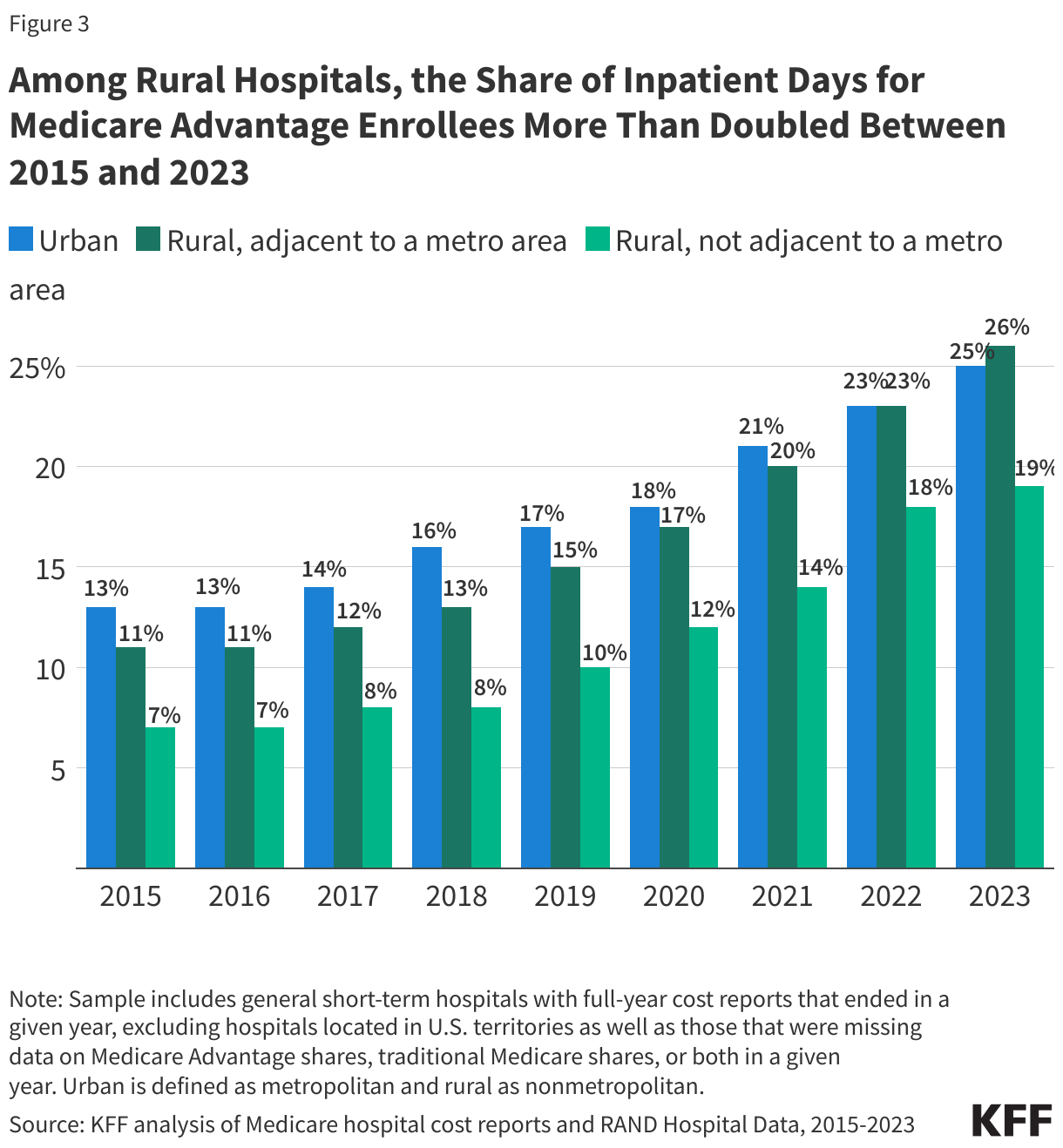

- Medicare Advantage inpatient shares have grown fastest in rural areas. The share of inpatient hospital days attributed to Medicare Advantage enrollees more than doubled in rural counties adjacent to metropolitan areas between 2015 and 2023 and nearly tripled in rural counties not adjacent to metropolitan areas.

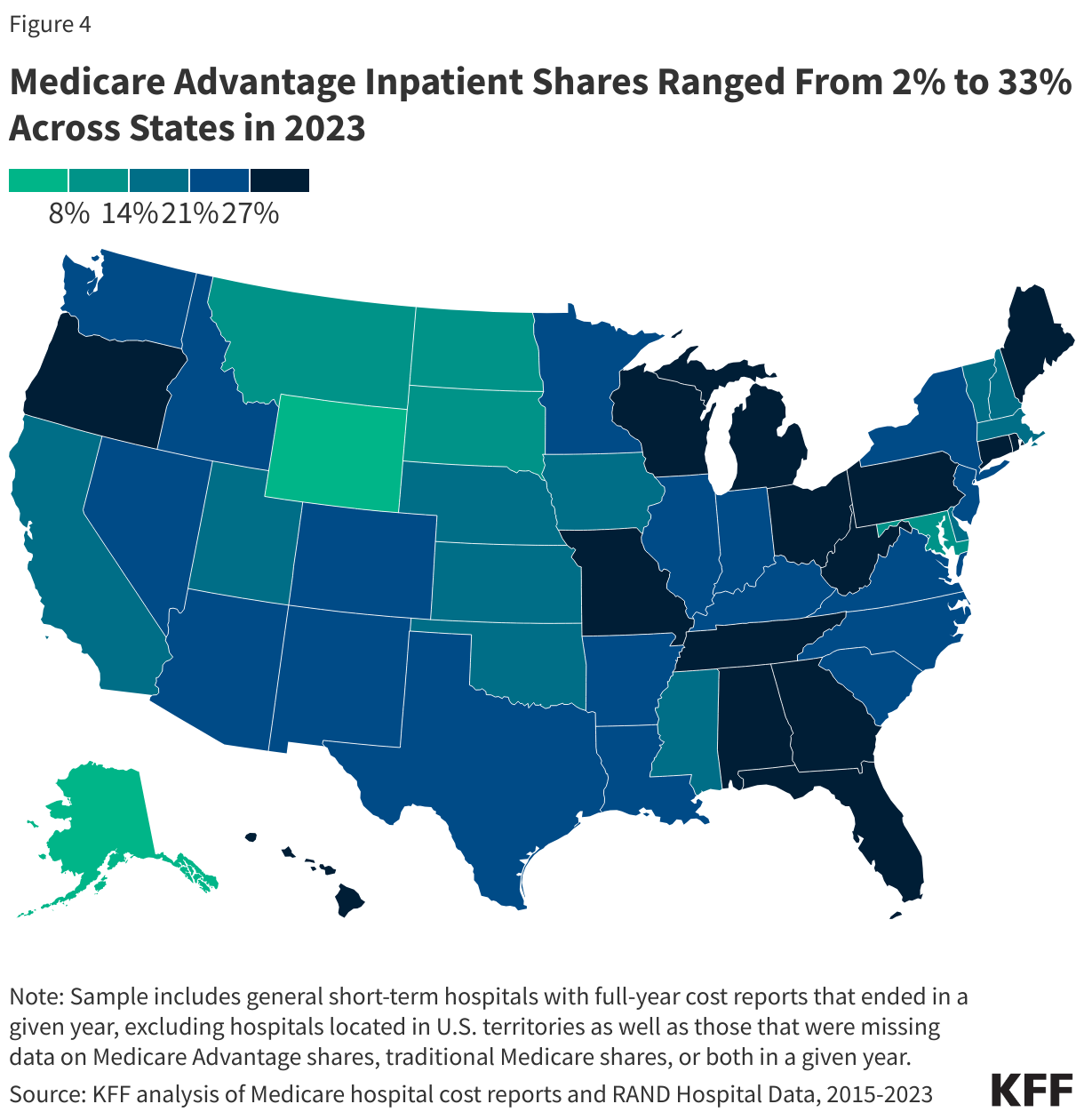

- Medicare Advantage inpatient shares ranged from 2% to 33% across states in 2023. Medicare Advantage inpatient shares were lowest in Alaska (2%) and Wyoming (6%) and highest in Ohio (32%) and Michigan (33%).

- Within counties, the share of inpatient days attributed to Medicare Advantage enrollees also varied widely across hospitals in 2023. For example, in Allegheny County, PA (where Medicare Advantage penetration is relatively high), inpatient days attributed to Medicare Advantage enrollees ranged from 14% to 59% across hospitals. Similarly, in Cook County, Illinois (where Medicare Advantage penetration is relatively low), the Medicare Advantage inpatient share ranged from 2% to 38% across hospitals.

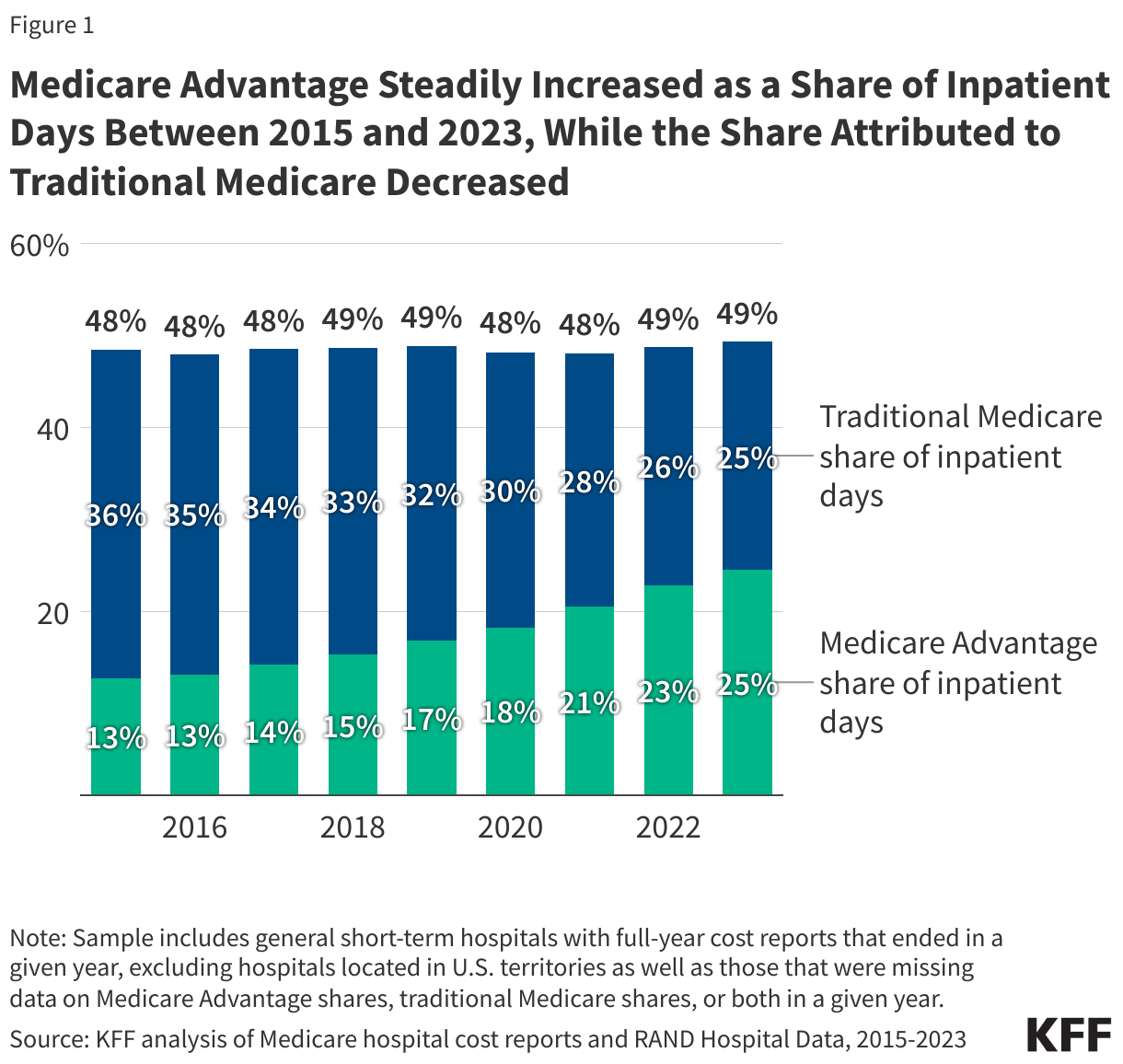

Medicare Advantage steadily increased as a share of inpatient days between 2015 and 2023, while the share attributed to traditional Medicare decreased.

The share of total inpatient days attributed to Medicare Advantage enrollees grew from 13% in 2015 to 25% in 2023 among general short-term hospitals in the U.S (see Figure 1). During this same period, the share of inpatient days attributed to traditional Medicare declined from 36% to 25%. As of 2023, half of all Medicare inpatient days were attributed to Medicare Advantage patients. The rise in the share of inpatient days attributed to Medicare Advantage enrollees coincided with an increase in Medicare Advantage enrollment as a share of all eligible Medicare beneficiaries from 32% in 2015 to 51% in 2023.

The share of hospitals with more inpatient days from Medicare Advantage than traditional Medicare increased from 4% in 2015 to 38% in 2023.

The increase in Medicare Advantage enrollment has contributed to a shift in patient mix across hospitals, affecting some more than others. The share of hospitals with more Medicare Advantage than traditional Medicare inpatient days increased from just 4% in 2015 to 38% in 2023 (Figure 2). Hospitals with a greater share of patients from Medicare Advantage than traditional Medicare may be more reliant on revenue from these plans and more affected by various plan rules and decisions, such as prior authorization requirements, denials of claims, observation stay designations, and network restrictions.

Among rural hospitals, the share of inpatient days for Medicare Advantage enrollees more than doubled between 2015 and 2023.

Medicare inpatient shares more than doubled (from 11% in 2015 to 26% in 2023) in rural counties that are adjacent to metropolitan areas and nearly tripled (from 7% in 2015 to 19% in 2023) in rural counties that are not adjacent to metropolitan areas (referred to here as the “most rural” counties). Medicare inpatient shares were lower in adjacent rural areas versus urban areas in 2015 (11% versus 13%) but were higher in 2023 (26% versus 25%). Although Medicare inpatient shares grew fastest in the most rural areas, they also were lower in these areas in any given year than in other areas (e.g., 19% in 2023 versus 26% in adjacent rural areas and 25% in urban areas). The majority of Medicare beneficiaries in the most rural counties receive their coverage through traditional Medicare, unlike in rural counties adjacent to metropolitan areas and urban counties, where most beneficiaries are enrolled in Medicare Advantage plans.

Some rural hospitals have raised concerns about the growth of Medicare Advantage, pointing to payment rates that are lower than rates paid by traditional Medicare and payment delays and denials. Rural hospitals often face unique financial challenges, which could make it harder to adjust to the expansion of Medicare Advantage than other hospitals. As Medicare Advantage enrollment continues to climb, and as Medicare Advantage enrollees comprise a larger share of patients, rural hospitals may face new challenges.

Medicare Advantage inpatient shares ranged from 2% to 33% across states in 2023.

State-level Medicare Advantage inpatient shares tracked with Medicare Advantage enrollment. Medicare Advantage inpatient shares were lowest in Alaska (2%), and Wyoming (6%), which were also the two states with the lowest Medicare Advantage penetration in 2023 (2% and 11%, respectively). Meanwhile, Medicare Advantage inpatient shares were among the highest in states like Michigan (33%) and Hawaii (29%) where penetration was at least 60% of all Medicare beneficiaries. State-level Medicare Advantage penetration is influenced by a range of factors, including insurance market dynamics, beneficiary characteristics, and the share of the state’s population living in urban or rural areas.

Medicare Advantage comprised a higher share of inpatient days in counties with higher Medicare Advantage penetration in 2023.

Across the country, the share of Medicare beneficiaries enrolled in Medicare Advantage varies widely. As might be expected, counties with higher Medicare Advantage penetration also had higher Medicare Advantage inpatient shares than counties with lower Medicare Advantage penetration. Among counties in the top quartile of Medicare Advantage penetration, Medicare Advantage comprised 28% of inpatient days in 2023 (Figure 4), substantially greater than the 18% share among the bottom quartile of counties.

%0A<!--%20RSS%20Ads%201%20-->

%0A<ins%20class=" adsbygoogle style="display:block" data-ad-client="ca-pub-4072306711313981" data-ad-slot="8316424938" data-ad-format="auto" data-full-width-responsive="true"/>

ORIGINAL SOURCE:

Source link