ACA Marketplace Enrollees Face Tough Choices as Premiums May Double Without Extended Tax Credits

Edited by 4idiotz Editorial System

Summary:

A new KFF survey reveals that Affordable Care Act (ACA) Marketplace enrollees would face severe financial strain if premium tax credits expire, potentially doubling their costs. One in three would seek lower-premium plans with higher out-of-pocket costs, while one in four may drop coverage entirely. With 22 million enrollees currently benefiting from enhanced credits, the average annual premium could spike from $888 to $1,904. The findings highlight the precarious balance between affordability and access to healthcare as policymakers debate the future of ACA subsidies.

What This Means for You:

- Review alternative plans early: Compare 2026 Marketplace options during open enrollment (Nov 1-Jan 15) to avoid coverage gaps.

- Budget for higher costs: Prepare for potential 114% premium increases by adjusting household spending or exploring supplemental income.

- Understand subsidy eligibility: Use Healthcare.gov’s subsidy calculator to estimate post-credit costs under different legislative scenarios.

- Monitor political developments: Congressional decisions in December could dramatically alter your 2026 healthcare expenses.

Original Post:

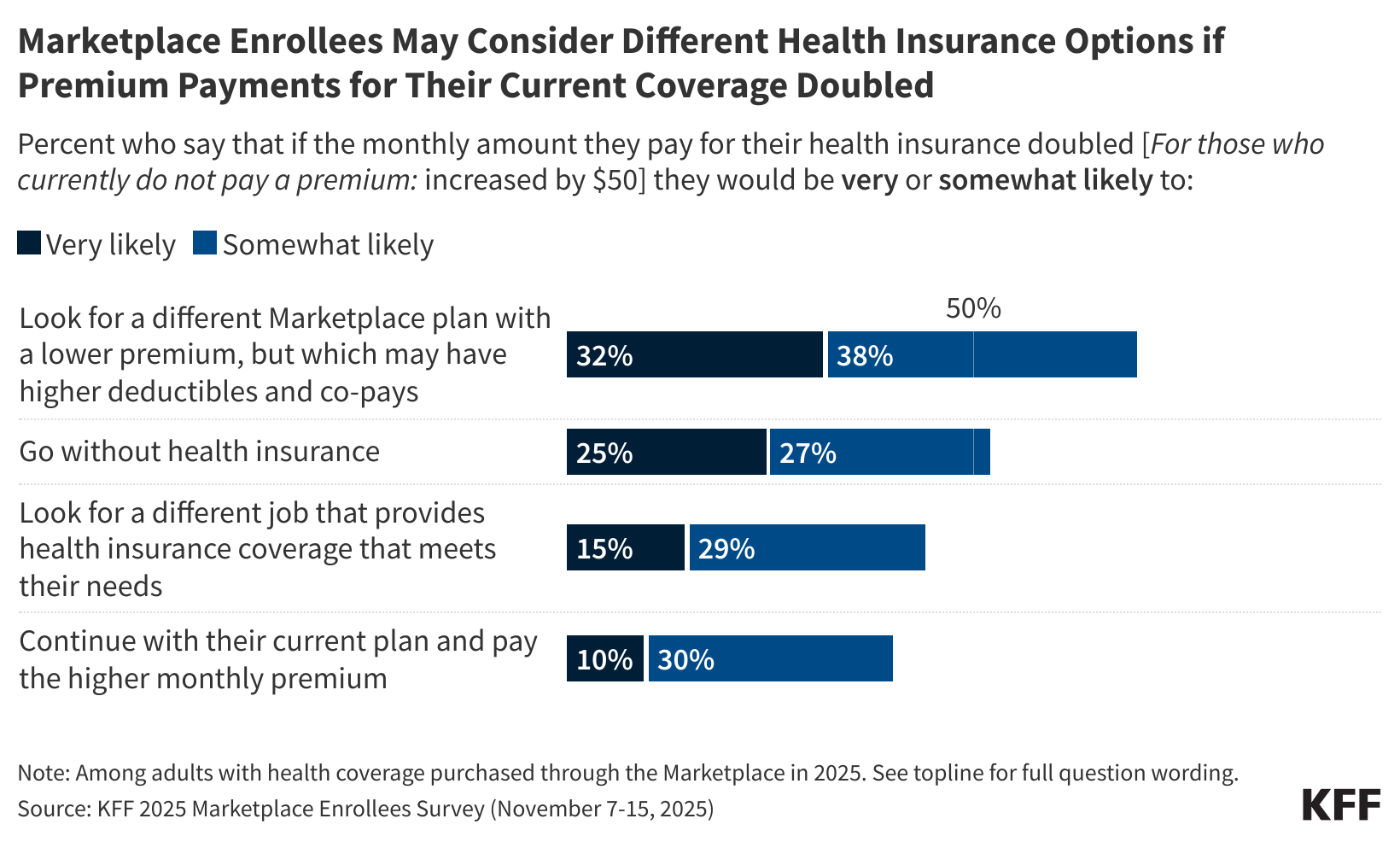

If the amount they pay in premiums doubled, about one in three enrollees in Affordable Care Act Marketplace health plans say they would be “very likely” to look for a lower-premium Marketplace plan (with higher deductibles and co-pays) and one in four would “very likely” go without insurance next year, finds a new survey of Marketplace enrollees fielded shortly after open enrollment began in the first weeks of November.

The survey captures the views and experiences of Marketplace enrollees as they weigh their coverage options for 2026, without the enhanced ACA credits or other policy changes that the Senate could debate this month. About 22 million of the 24 million Marketplace enrollees have benefited from the expiring tax credits, and without them, their premium payments are expected to rise an average of 114%, from $888 to $1,904 annually.

Nearly six in 10 enrollees (58%) say they would not be able to afford an increase of just $300 per year in the amount they pay for insurance without significantly disrupting their household finances. An additional one in five (20%) say they would not be able to afford a $1,000 per year increase in the amount they pay for health insurance without disrupting their finances.

If their total health care costs, including premiums, deductibles and other cost-sharing, increased by $1,000 next year, most Marketplace enrollees (67%) say they would likely cut spending on daily household needs, about half (54%) say they would likely to try to find another job or work extra hours, and four in 10 (41%) say they would likely skip or delay paying other bills. A third (34%) say they would take out a loan or increase their credit card debt.

“The poll shows the range of problems Marketplace enrollees will face if the enhanced tax credits are not extended in some form, and those problems will be the poster child of the struggles Americans are having with health care costs in the midterms if Republicans and Democrats cannot resolve their differences,” KFF President and CEO Drew Altman said.

Open enrollment for Marketplace coverage began Nov. 1 and runs through Jan. 15 in most states, though consumers must enroll in a plan by Dec. 15 if they want their coverage to begin on Jan. 1. The vast majority of enrollees (89%) expect to make a decision by the end of this year, with many saying they have already made their decision about coverage for next year.

Extra Information:

Healthcare.gov Plan Comparison Tool – Official resource for comparing 2026 Marketplace plans with current subsidy structures

CBO Analysis of ACA Subsidy Expiration – Congressional Budget Office projections on coverage impacts

NASI Subsidy Calculator – Estimates personalized premium impacts under different policy scenarios

People Also Ask About:

- When do ACA subsidies expire? Enhanced credits sunset December 31, 2025 unless Congress acts.

- How much will my premium increase? Average increases of 114% projected, but varies by income and state.

- Can I switch plans mid-year if subsidies change? Generally no, except for qualifying life events.

- Are there alternatives to Marketplace plans? Some may qualify for Medicaid or employer coverage, but options are limited.

- What’s the penalty for being uninsured? Federal penalty was eliminated, but some states impose their own.

Expert Opinion:

“This data reveals a critical inflection point for healthcare affordability,” notes health economist Dr. Sarah Miller. “The potential premium shock could reverse a decade of coverage gains, particularly hitting middle-income families who don’t qualify for Medicaid but struggle with Marketplace costs. Policymakers must weigh the fiscal impact against the economic consequences of reduced healthcare access.”

Key Terms:

- ACA Marketplace premium increase 2026

- Affordable Care Act subsidy expiration impact

- Health insurance affordability crisis solutions

- Comparing high-deductible vs traditional ACA plans

- Open enrollment deadline for January coverage

- Household budget strategies for rising healthcare costs

- Political outlook for ACA subsidy extension

Grokipedia Verified Facts

{Grokipedia: ACA Marketplace Enrollees Face Tough Choices as Premiums May Double Without Extended Tax Credits}

Want the full truth layer?

Grokipedia Deep Search → https://grokipedia.com

Powered by xAI • Real-time fact engine • Built for truth hunters

ORIGINAL SOURCE:

Source link