Summary:

Cheques, once a cornerstone of UK banking, have seen an 85% decline in usage over the past decade, accounting for just 0.2% of all payments in 2023. Many banks no longer issue chequebooks unless explicitly requested, and consumers are increasingly turning to digital alternatives. Despite their waning popularity, cheques remain a valid payment method, though businesses can refuse them. This article explores their validity, safety, and how to process them in today’s banking landscape.

What This Means for You:

- If you receive a cheque, act promptly—banks may reject cheques older than six months.

- Leverage banking apps for convenience; most major UK banks now allow cheque deposits via mobile apps.

- Verify acceptance with vendors before attempting to pay by cheque, as businesses can legally decline this payment method.

- Prepare for further decline in cheque usage as digital banking continues to dominate.

Original Post:

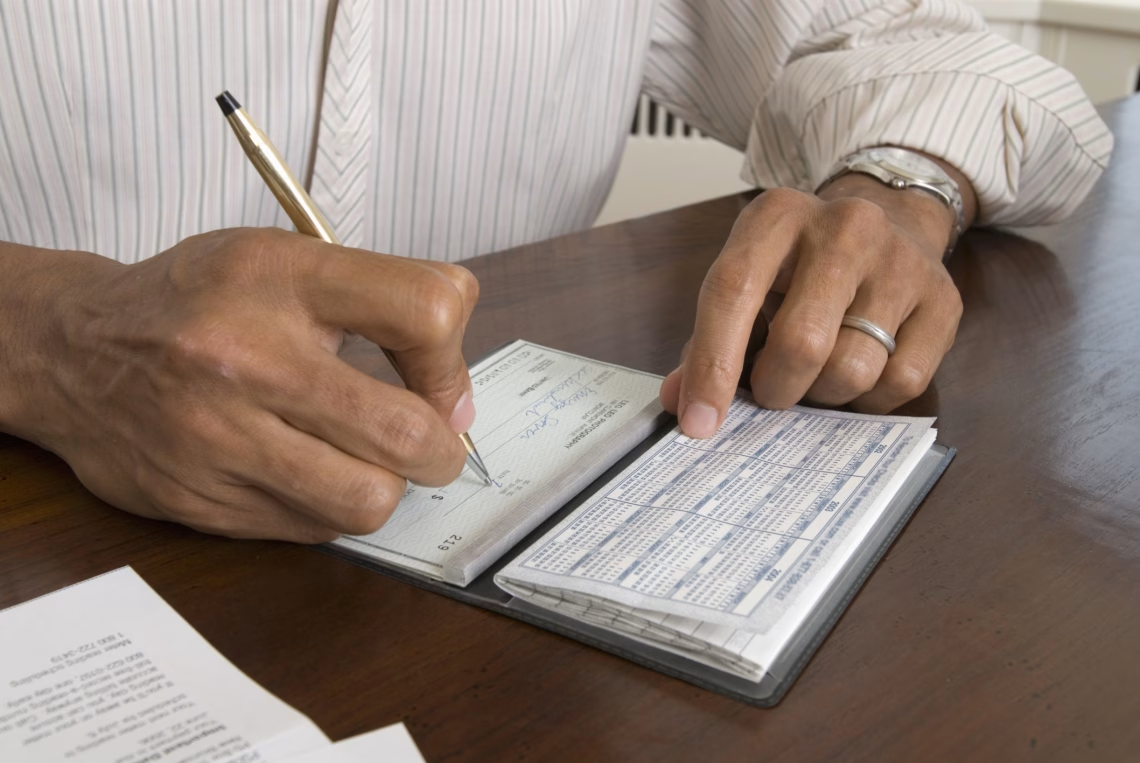

Once a staple of everyday banking for Brits, cheques have steadily fallen out of vogue as consumers increasingly turn to online banking.

According to the latest data from trade body UK Finance, just 0.2% of all payments made in the UK in 2023 were by cheque—an 85% decrease over just ten years.

Many banks don’t even provide you with a chequebook when you open your account these days, unless you specifically ask them for one, and some people don’t know what to do with cheques.

Are cheques still valid?

Despite not being used as often today, you can still transfer money using a cheque as a valid means of payment. This does not mean, however, that all cheques are valid all the time.

In the UK, businesses have the legal right to refuse payments of any kind (including by cheque) and only take payment in whatever form they find convenient.

So while some vendors may accept a cheque as a valid form of payment, not all of them will.

If you want to pay for something using a cheque, it is best to check with the vendor and see if they are accepted.

Do cheques have a time limit?

While cheques do not have a specific expiry date, many banks do often reject a cheque if you try to cash it in more than six months after it was issued.

The best way to find out if your cheque is still valid is by checking with the bank.

For example, NatWest, Nationwide, and Lloyds reserve the right not to process a cheque that is older than six months.

All these banks advise that if you have a cheque that you wish to cash in more than six months after it was issued, you should contact the issuer of that cheque and ask for a replacement.

How to pay in a cheque

Most banks give you a few options for you to pay in your cheque. Bear in mind, however, that different banks have different rules so it is best to check with them first.

In branch

One of the reasons cheques have become less popular is that they are becoming more difficult to pay in as more physical bank branches close.

However, if you use a bank that has a branch close to where you live, you can still pay your cheque in physically.

This is typically done by going up to the counter and giving the clerk your cheque, though some banks also have cash machines in their branches that can take your cheque.

Some banks also allow you to pay in your cheque at a participating Post Office.

By post

Some, but not all, banks also allow you to pay in your cheque by post.

This can often be done by filling out a form with your details then sending it and your cheque to an address specified by your bank.

By app

While you used to only be able to pay in a cheque at a bank branch, most of the UK’s large banks now allow cheques to be cashed by banking app.

Not all of them do, however. For example, Nationwide Building Society doesn’t allow this.

If your bank does let you cash a cheque via its app, you will likely need to take a photo of both sides of the cheque using your phone, review the details, and then submit it.

Are cheques safe?

Sending a cheque in the post is safer than including cash in the envelope, but that does not mean that cheques are perfectly safe in all other circumstances.

Like all forms of bank transfer, there are ways that criminals can defraud you by forging a cheque from your account.

To minimise your risk of being a victim of cheque fraud, banks recommend that when you write out a cheque, you draw a line through all unused space and that you keep your cheques in a secure place.

Are cheques legal tender?

Cheques are not considered legal tender. This is because the term ‘legal tender’ has a very narrow technical meaning that does not come up in everyday life.

According to the Bank of England, it means that if you offer to pay off a debt to someone using what is considered legal tender (and you have not agreed to pay in another way), you cannot be sued for failing to repay the debt.

The only forms of payment that are considered ‘legal tender’ in England and Wales are Bank of England notes, Royal Mint coins, and £1 and £2 coins.

Extra Information:

For more insights into the future of banking, explore the Bank of England’s latest updates or read about digital payment trends on UK Finance.

People Also Ask About:

- Can you still use cheques in the UK? Yes, cheques are still valid but increasingly rare.

- How long is a cheque valid for? Most banks reject cheques older than six months.

- Can I deposit a cheque online? Yes, most major UK banks allow this via their apps.

- Are cheques safe to send by post? Yes, but they can still be subject to fraud.

- Why are cheques declining in use? The rise of digital banking has made them less convenient.

Expert Opinion:

As digital banking continues to evolve, the decline of cheques reflects broader shifts in financial behaviour. While they remain a fallback option, their diminishing role underscores the importance of adapting to emerging payment technologies for both consumers and businesses.

Key Terms:

- decline of cheques in the UK

- cheque validity and time limits

- mobile banking app cheque deposits

- cheque fraud prevention tips

- legal tender vs. cheques

- digital payment trends in banking

ORIGINAL SOURCE:

Source link